Comparing US vs European living standards

Constant PPP is more robust than current PPP, and better matches endogenous divergence.

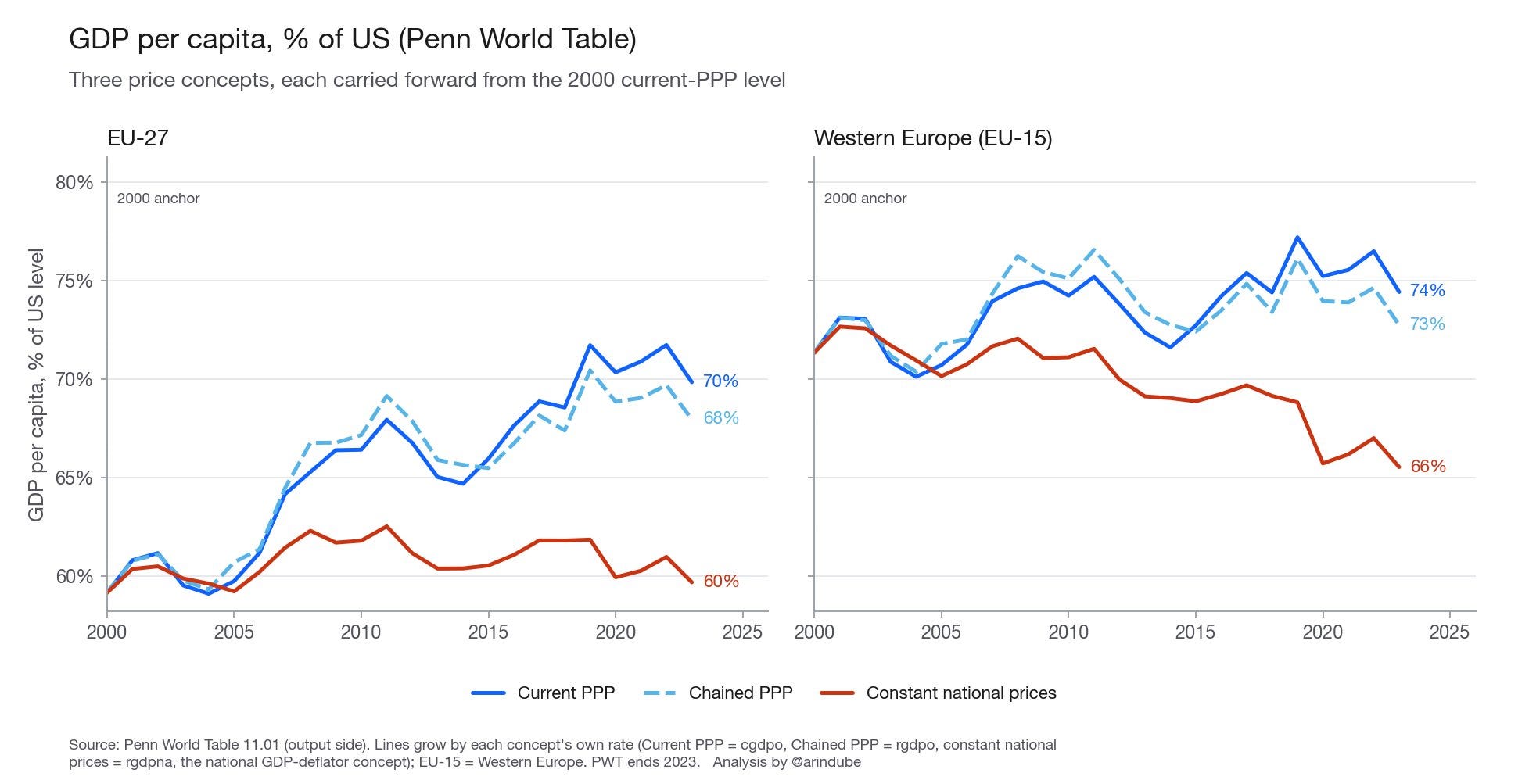

Krugman kicked off this tournament via his recent infamous post stating that Western Europe's (EU-151) GDP per capita has not declined (relative to the US) this century so far. Once you adjust for (current or chained) PPP2, you derive this result which is somewhat contrarian to the current prevailing pessimistic narrative on European living standards. If we compare the broader EU-27 to the US, then we actually observe a slight rise. Only via holding national price levels constant (equivalent to GDP deflators) do you get an EU-15 relative decline, and EU-27 stagnation.

Garicano, Aghion, and Bergeaud emphasise that America holds a clear advantage on productivity growth, the frontiers of output such as the tech industry, and business dynamism. This generates meaningful and substantial spillovers to Europe via falling prices and gains to consumer surplus (I, as a European, am using a smartphone to write this on Substack at zero fixed or marginal cost3 after all!). However, the labour-market gains in wages and employment in these industries are disproportionately concentrated at the headquarters and labs of these frontier industries, owing to agglomeration effects (which themselves occur at the domestic nation). These benefits are non-tradeable, and so America disproportionately gains relative to the rest of the world. To argue otherwise would be tantamount to claiming that growth in the US tech industry benefits the Bay Area and the Rust Belt equally4!

The other day on X, I stumbled across this paper. As Romer emphasised in his work on endogenous growth theory, technology diffusion across countries (and more recent work examining diffusion within countries between ‘frontier’ vs ‘laggard’ industries5) is not instantaneous. Gains to TFP in America take time to spillover into Europe. This causes TFP growth to be higher in America at any given point in time, and these differences compound over time. Krugman highlights a convergence that tends to dissipate once accounting for endogenous growth dynamics: a point that he's all too-aware of, of course…

On a more technical note, we shouldn't necessarily rely on current PPP comparisons as they emphasise purchasing power today. This bias towards the present neglects the productivity growth and price changes accruing over time. Therefore current measures tend to exclude much of the gains arising from (relative) growth. Using a base year to hold prices constant is a better means of capturing these dynamics, despite treating a non-constant variable as constant at a somewhat arbitrary moment in time. Yet no matter which base year you choose, the divergence tends to arise, therefore constant PPP is a more robust measure too.

Of course, international measurement only gets harder from here. When estimating inflation domestically, you require changes to consumption bundles and the quality of the goods and services within. For PPP, you must repeat this exercise for these differences in representative bundles across countries at the same point in time. Simply put, a reasonable prior is that you lose precision via switching from national deflators (which constant PPP is equivalent to) to current PPP. Product sampling and quality adjustment techniques of course differ cross-country. In Britain, the HMRC payroll data vs the ONS’ surveys imply entirely different dynamics for GDP per hour growth, so even statistical agencies within a country disagree!

However, these deflators tend to neglect convergence in tradeables prices. PPP eliminates international price differences for tradeables as a result of exchange rates: best emphasised by The Economist's Big Mac Index. Nonetheless this adjustment is only really valid for tradeables, and non-tradeables form a large proportion of our economies. The Krugman camp is adjusting by using a measurement ill-equipped to answer the questions they're asking. Nonetheless, we can disaggregate the national accounts, and this does not seem too empirically relevant overall. PPP falls faster than the prices of tradeables and this pattern reverses for non-tradeables, and these roughly offset. Again, whilst Krugman's point may be valid for the tradeable sector, Garicano et al are correct with respect to non-tradeables, which form a larger share of both our economies.

In any case, the fact that America leads Europe in terms of productivity growth is not really in dispute6. Ultimately, it’s this variable that determines growth and hence differences in living standards across countries. Indeed, this advantage is the most robust point emphasised throughout this debate.

Yes this debate excludes the countries outside the EU. On average, Western European non-EU nations tend to be richer (Switzerland, Norway, Liechtenstein, etc) than EU equivalents and Eastern non-EU poorer. If we're weighting by population, then the UK (whose standards are closer in line to the EU-15 average) attenuates this divergence. Hence overall tracking EU GDP measures provides a close proxy for the living standards of Europe overall.

If you adjust for hours worked, then their respective living standards are actually broadly equivalent. However Europe's ageing population is itself an economic issue, and Prescott (2004) shows that higher leisure consumption in Europe is probably a function of distortionary taxes and transfers more than income effects from exogenous labour-supply preferences. For these reasons I do not accept as valid adjustments for hours worked.

In the budget constraint, and abstracting from opportunity costs in the time constraint!

Ironically it was Krugman (1991) himself that won the Nobel in large part for his work on geographic agglomeration differences…

Krugman spent the last decade and a half attributing this divergence to insufficient demand, despite endogenous growth being primarily a supply-side theory: determined by capital investments generating “learning via doing” and IRTS, supply of human capital, supply of ideas, etc. To advocate for his Keynesianism, he’s aware of this empirical observation, yet tacitly backtracks on this point in this debate. His reasoning is not internally consistent, and I suspect we all know the reason why…

Neither in dispute is the fact that this growth is concentrated within a few frontier sectors: tech a prime example. This debate also boils down to estimating the magnitude of spillovers, to what extent they affect prices vs quantities, and scale assumptions (the compounding growth divergence only holds if tech gains produce IRTS dynamics). In effect, we're debating which growth model specification is best calibrated.

This is interesting but I'm not sure that one Ed Prescott paper is sufficient to reject adjusting for hours worked out of hand.

But I'd be interested in whether lower hours worked could reflect unemployment or barriers to labour market entry, rather than folks clocking off at five and taking a nice amount of holiday.